New York State Senator Gustavo Rivera at the launch of a campaign to end the privatization of home care on December 11. (Ilana Berger)

December 11 dawned rainy and cold, but the rhetoric was heated at the Open Door Senior Center in New York City’s Chinatown.

At stake was a major question: could those gathered stop the state from continuing to give billions of dollars to private insurance companies to provide home care for older and disabled New Yorkers?

New York State Senator Gustavo Rivera at the launch of a campaign to end the privatization of home care on December 11. (Ilana Berger)

“You’ve heard it said that somehow privatization makes things better. But it does not!” thundered State Senator Gustavo Rivera to loud applause from 100 or so activists in attendance. Rivera, chair of the Health Committee continued, “This is a failed experiment. One we have to do away with, and the way we’ll do it is to pass this bill.” Alongside Rivera were some of New York’s most prominent legislators who were there to introduce The Home Care Savings & Reinvestment Act.

State Senator Jessica Ramos focused on the big picture: “This doesn’t just save us $3 billion a year. It starts to shift the paradigm of how we deal with health care.”

But how did long term care for those on Medicaid come to be a profit-making business? How well or poorly does the system serve those in need? And what does today’s privately managed home care landscape look like from ground level?

Mother’s Day, 2018

Five years ago, Jennifer Wulfe was finally getting her mother, Dinah Kiely, out of a nursing home in Kingston, New York.

After months of struggling with the home, Wulfe was able to take Dinah, then age 71, off a medication that caused a dementia-like condition, and now her mother was acting more like herself. Though she needed a walker due to breaking a bone in her lower back, Wulfe was determined to take her to their home in Cottekill, a tiny village in the Mid-Hudson region of New York.

Jennifer Wulfe’s mother Dinah Kiely in 2021. (Caring Across Generations)

As a single mom of twin teens, and juggling three part-time jobs, Wulfe knew she would need home care help. Her mother qualified for home care through the state’s Medicaid program, however, the process of obtaining a Medicaid home health aide was unclear to Wulfe. When she checked her mother out of the nursing home, Wulfe was handed a list of company names and told to pick one to arrange for care.

“I didn’t know what name to pick,” says Wulfe. “There’s no one to tell you or guide you.” She chose Hamaspik Choice, a company she had never heard of, but which began a fraught relationship with one of the 24 private insurers designated by the state to manage people’s long-term care.

It wasn’t always this way

Corporate management of Medicaid home care is a relatively new phenomenon. Until recently, states managed this kind of care themselves. In New York, just over a decade ago most Medicaid dollars for home care were allocated to counties and disbursed based on “clinical need,” says Domenic Colavito, the co-founder and chief operating officer of OurCare, an in-home care agency with one office in New York and one in Florida. They have 15 internal employees and employ 350 home care aides. OurCare is one of more than 1500 agencies that provide home care services in New York.

Colavito has lived through the home care experience. After his father was diagnosed with stage 4 lung cancer in 2010, Colavito became his father’s full-time caregiver. Since then, Colavito has witnessed first-hand the transition of home care from a public good to a private industry profit. He and a partner founded OurCare in 2012 when New York was transitioning to corporate managed in-home care.

Domenic Colavito, co-founder of OurCare In Home Health Services. (Domenic Colavito)

Before the early 2010s, Colavito says, “The [county] clinicians would look at the chart for these patients, and say, okay, this person is 80 years old, a fall risk, has dementia, let’s give them 24/7 care. What happens now is a clinician from these MLTCs [Managed Long Term Care companies] will look at that same exact chart and say, what’s the least amount of hours I can give them, so we can make money. They’re driven by profits.”

In exchange for making determinations about home care service, MLTCs receive a fixed amount per patient from the New York Department of Health: about $5,000 per person, per month. Colavito says MLTC reps have told him that if a patient gets more than 30 hours of home care a week, it’s “a loss for these companies … regardless of the clinical need.”

Nationwide, the momentum behind the privatization of government services has been building for decades. In the case of long-term home care, corporate insurers began to take over in most states by the 1990s. In 2013, state officials in Connecticut made a bold move in the opposite direction, becoming the only state to have extricated itself from private insurers and gone back to a public system. Today, only three states (Washington, Alabama and Connecticut) manage such care without the layer of private insurance. If the Home Care Savings & Reinvestment Act succeeds, New York will follow in Connecticut’s path-breaking footsteps.

Clinical need vs. private profit

Over the past several years, Wulfe and her mother suffered from inadequate coverage of their care needs. Wulfe’s MLTC, Hamaspik Choice, could take weeks or even months before approving home care hours, and then only approved “so few hours, it really didn’t make much difference,” Wulfe says.

Wulfe tried to get her mother into a day program, to enjoy a little social life, only to be told there were none. She found out later there were in fact day programs nearby but “none associated with my MLTC,” she says. The managed care plan would “constantly reject and reject” her mother’s dental claims and her mother would “live on Tylenol for dental pain” until their dentist’s office could finally win an approval. “They just did very little for me,” says Wulfe.

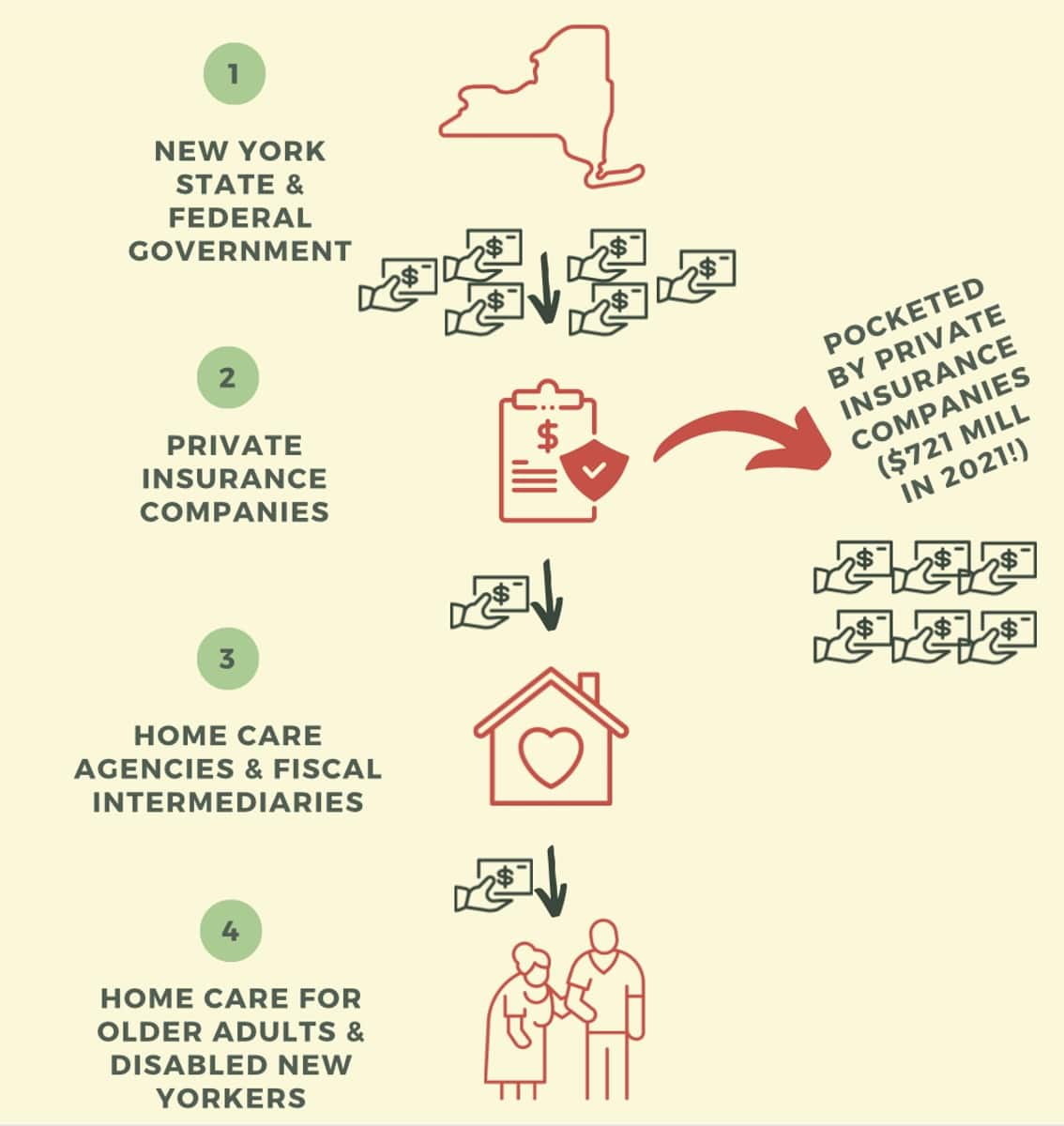

How money flows in managed long-term care. (NY Caring Majority)

Meanwhile, Hamaspik Choice did well for itself. The Executive Director’s pay exceeded $500,000 according to 2021 tax filings. Other managed care firms in New York did even better. Consider Fidelis Care, founded in New York City in 1993 as a Catholic-run, tax-exempt, not-for-profit HMO. The company grew quickly after an experienced healthcare executive named Mark Lane was brought in. In just over a decade, Lane turned the fledgling operation into the largest manager of state Medicaid services. By 2012, Fidelis had 750,000 members in New York, and Lane was earning nearly $2 million a year. As the New York Post cheekily put it, “that’s a lot of pennies from Heaven.” They also pointed out that virtually all of Lane’s earnings were taxpayer pennies.

The pennies kept raining down. In 2018, multinational insurance giant Centene swallowed Fidelis for $3.75 billion. By 2023, Fidelis Care could boast that one out of 9 New Yorkers were members of their various health plans, including a major MLTC division. Centene had clearly made a sound investment.

How did managed care companies do so well on the public dime? One answer is revealed by scores of online comments from anguished care recipients. For example, Jessica H. posted this one-star review of Fidelis on the Better Business Bureau site in early November. Her mother had been approved in August for 5 hours a day of home care through Medicaid. Yet months later, no care was forthcoming:

If I could give 0 stars I would. I’ve been BEGGING for [home] care for my sick mom since August. These people don’t know what they’re doing. If I could go back I would NEVER CHOOSE FIDELIS AGAIN. They don’t want to help people who NEED help.

The poor review is no anomaly. Despite its A+ rating from the BBB, the company has an average of 1.24 stars out of five from 34 reviews on this website.

As critics of the system have noted, Fidelis and other MLTCs know exactly what they’re doing. They have a potent incentive that goes over and above care: the profit motive. Go to virtually any review site and the verdict on Fidelis and other MLTCs—with few exceptions—is remarkably consistent. Commenters report they are “horrible,” “unresponsive,” “a total scam.”

Another factor is a lack of state oversight. “There’s no auditing, they’re not regulated in any way,” Colavito says. He tells horror stories of MLTCs that have stiffed his agency. They “systematically create billing delays and keep 100% of the Medicaid money that they received from the state, and have zero ramifications, as though they’re not breaking any rules.”

Meanwhile, the MLTCs reap rewards. In 2021 alone, these insurers made a total of $721 million in profits.

Fidelis did not respond to requests for comment, and it gives boilerplate responses to online complaints. An official from Hamaspik Choice responding in an email wrote, “As a provider-sponsored managed long term care plan, we are committed to our mission, which is always embedded in our work – to strive for excellence in providing access to quality-driven health care coverage, in a culturally sensitive, timely and responsive manner.”

The struggle for fair pay for home care

The people who need home care and the small home care agencies that provide those services are by no means the only victims of a profit-based system. While executives and shareholders of managed care companies grow wealthy, home care workers remain poorly paid. In New York 42% of them live at or near poverty.

Yet in recent years, a growing movement has sought to push back against the profit motive. In 2015, a coalition of workers, family caregivers, people with disabilities, seniors and activist groups formed the New York Caring Majority. One of their key goals: raise awareness of the way poverty-level pay was causing severe worker shortages and widespread suffering for those who can’t get enough care. Soon the core group was joined by home care agencies, independent living centers and unions including SEIU local 1199. Today, over 120 organizations are allies.

The Caring Majority’s signature legislation, Fair Pay for Home Care, won over a majority of state representatives. (Full disclosure: The present writer is a member of the New York Caring Majority.) The Fair Pay Act called for home care workers to receive 150% of the minimum wage. But a roadblock was New York’s Democratic governors—first Andrew Cuomo, then his successor Kathy Hochul. In 2022, after a relentless pressure campaign, compromise was reached: home care workers paid under state Medicaid would get $2 above the minimum wage by October, 2022 and $1 more, 12 months later. It wasn’t the full loaf, but it was a significant win.

The activists were pleased, and vowed to continue fighting for the full pay increase. But what happened next was worse than they expected.

“It was totally outrageous”

“In the summer of ’22, we started to hear alarming things from our friends in the home care provider community,” says Ilana Berger, a Caring Majority organizer and New York Director of the nonprofit Hand in Hand.

Ilana Berger of the New York Caring Majority and Hand in Hand. (Ilana Berger)

Home care agencies reported that MLTCs were stonewalling the pay increase, even though the insurers were in line to get Medicaid money to pay for it. Meanwhile, the agencies were required by law to pay the increase. They calculated that the initial $2 an hour raise for home care workers would cost them the $2, plus an additional 66 cents an hour to break even, with taxes, benefits and other expenses. But the MLTCs, in some cases, were offering as little as 20 cents extra. “Not $2.20,” says Berger, “But like 20 cents, literally. It was totally outrageous.”

Domenic Colavito, who ran one of those home care agencies, was worried about getting squeezed. He already limited his home care business to one-third Medicaid patients, calling it a “loss leader.”

He explains, “If I stopped working with Medicaid, I’d make more money. But to be part of our community doesn’t mean just servicing rich people.” Ironically, it looked like the extra pay mandated for home care workers would put even more financial stress on his operation. “We 1,000% support caregivers getting more money. It’s just that [the money has to] come from somewhere.”

Colavito went to Albany with charts and graphs and tried to get the Hochul administration to address the problem of funds not being passed along. He wrote to them, in 2022, “small businesses like ours will be forced to discharge patients under these plans.” But, he says, “No one cared.”

Ilana Berger and her allies tried to intervene. They had meetings and calls with the state Department of Health. “It was bizarre,” she says. “I was on calls where the people who manage Medicaid were asking us and the providers to tell them how much the [MLTC] plans were paying. And we were like, that’s not our job, that’s your job! Something is out of control when the state is completely unwilling to hold the plans accountable.”

For their part, insurers continue to deny any culpability. In a radio interview aired on December 7 on Albany-based Capitol Pressroom, Joe Twardy, president of Nascentia Health, was asked whether their company and others withheld the added funds for home care workers. He replied, “To say that dollars are being held by the plans is categorically false.”

Changing winds

For five years, Wulfe cobbled together ways to care for her mother at home. Then there was a crisis. On July 7 this past summer, Wulfe got a call at work from her home care aide. Her mother was suddenly unable to move. After five days in a local hospital in Kingston they could not determine the cause, and she was brought to a different nursing home than before. According to Wulfe, it’s been a nightmare. “My mom’s crying in her bed in pain all the time,” Wulfe says. “They don’t dress her. They don’t shower her. She needs help eating but they don’t feed her. She can’t drink for herself, so she’s dehydrated.”

Wulfe petitioned Hamaspik for round-the-clock care so she could take her mother home. Hamaspik denied the 24/7 request, only willing to allow 65 hours a week. Desperate to get her mother out of the nursing home, Wulfe called around for advice. One friend told Wulfe that she could apply for a “waiver” from the state’s Nursing Home Transition and Diversion (NHTD) program that’s only available if your loved one qualifies for a nursing home but you prefer to care for them at home. The program bypasses the privatized system and is directly administered by a state agency. Wulfe filed the application in October.

Colavito is enthused about the NHTD waiver program, which began in 2007. “First and foremost, the clients get what they need,” he says. The program pays his agency well enough so that he can fully pay his workers, afford to give them overtime, keep the lights on and make a fair margin. “You have a positive environment because the caregivers can live and support themselves. And my business will be successful. If I could have every case like that, I would cry tears of joy.”

The “ideal solution,” for all of Medicaid home care, says Colavito, would be “exactly like the waiver program.” Ilana Berger agrees and adds, “There’s absolutely enough money to put billions more into home care if we had different priorities. If [the Home Care Savings & Reinvestment Act] eliminates the profit motive from home care delivery, it will bring back $3 billion a year.” Money, she says, that can be used to fully fund Fair Pay for Home Care workers, create more jobs to end the worker shortage, and serve people who need it most.

Next steps toward reform

“The funding that goes into the pockets of the insurance industry needs to come back to all of us,” said Senator Rivera at the event on December 11. He and Senator Ramos urged voters to make their voices heard. Rivera also warned that the insurance industry would “come out of the woodwork” and use their money and influence to fight back.

That was true in neighboring Connecticut, where it took several years to disentangle the state from Medicaid privatization. The state had been an early adopter of private insurers, starting in 1996, believing they would save money. But higher costs to the state began to surface and ugly denials of service to patients were exposed by advocates. Intense legal battles occurred, to try to force insurers to open their books. Meanwhile, anti-private industry fervor in the media and among the public added pressure. Ultimately, Connecticut ended privatization in Medicaid—all of Medicaid, not just long-term home care—in 2012.

Since then, the news out of Connecticut is positive. Medicaid per-member costs are down 14%. Administrative spending is only 2.8% versus a national average of 8.2%. Most importantly, care has improved. Preventative care is up 16%, hospital admissions down 6%, and ER usage down 25%. As one of Connecticut’s leading reformers, Sheldon Taubman, explained, “It has not been absolutely perfect. But, overall, it has been a dramatic improvement.”

Improvements to the system would have meant a lot to Wulfe and her mother. Dinah Kiely passed away the morning of December 19 while they were waiting for final approval of the waiver application.

When asked to reflect on all that she and her mother have gone through, Wulfe is quiet for a moment. “I’ve seen the horrors of getting older in this society,” she says, “So you just better stay healthy.”

Michael Solow’s work has also appeared in the New York Times, The River and the Albany Times-Union. He is a volunteer member of the New York Caring Majority and lives in Kingston, New York.

Have thoughts or reactions to this or any other piece that you’d like to share? Send us a note with the Letter to the Editor form.